Photos Courtesy of ONYXprj | iStock, GlobalData, Technavio Research, Adobe Stock #409611395, Research and Markets, Markets and Markets

Two major markets covered in Defense and Munitions, military manufacturing and firearm manufacturing, both expect to see continued growth heading into 2024, globally and in the United States. We’ve combed through various reports and this is what you can expect if your shop manufactures for the military or firearms industry.

Military

Global military spending is estimated to be $2.01 trillion in 2023 and expected to rise to $2.13 trillion in 2024, increasing at a 2.74% compound annual growth rate (CAGR) according to MarketsandMarkets. These increases could be a result of escalating military capabilities of China which have compelled neighboring nations to fortify their defense capabilities. The Middle East also contends with security threats emanating from terrorism, internal conflicts, and external aggression, prompting regional nations to allocate significant financial resources to safeguard their interests. Various regions around the world continue to confront distinctive security challenges, including territorial disputes, regional rivalries, and cross-border conflicts to help drive the defense manufacturing industry.

Missiles and missile defense

Precision strike missile capabilities and the modernization of air defense systems are driving the demand for missiles and missile defense systems (MMDS). The Russia-Ukraine conflict and heavy use of missiles and rockets by both countries have prompted other European countries to enhance missile and missile defense capabilities.

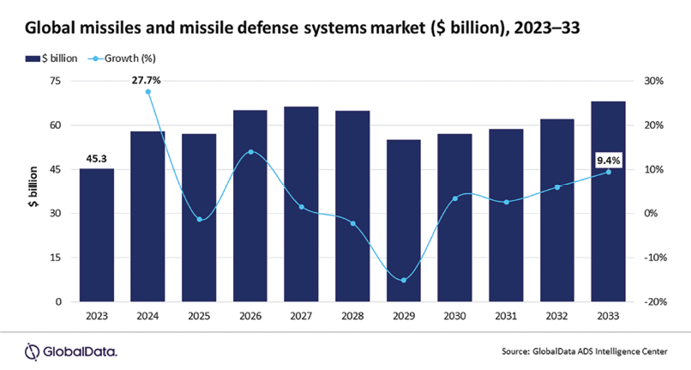

The global market for MMDS is forecast to grow from $45.3 billion in 2023 to $67.9 billion by 2033, according to GlobalData.

Their latest report reveals a 4.2% CAGR between 2023 and 2033. With Poland, Germany, and France prioritizing short-range and medium-range air defense systems along with man-portable systems such as Mistral, Piorun, and RBS-70 NG, Europe is anticipated to dominate the global MMDS market during the next decade with a 31.1% share.

The UK is developing an anti-ship missile with France under the Future Cruise/Anti-Ship Weapon (FCASW) missile program. This FCASW missile will replace the existing Exocet and Harpoon missiles from the French and Royal Navy’s arsenal. India and Russia, under the BrahMos collaboration, will be developing the hypersonic version of the BrahMos supersonic missile.

Rockets

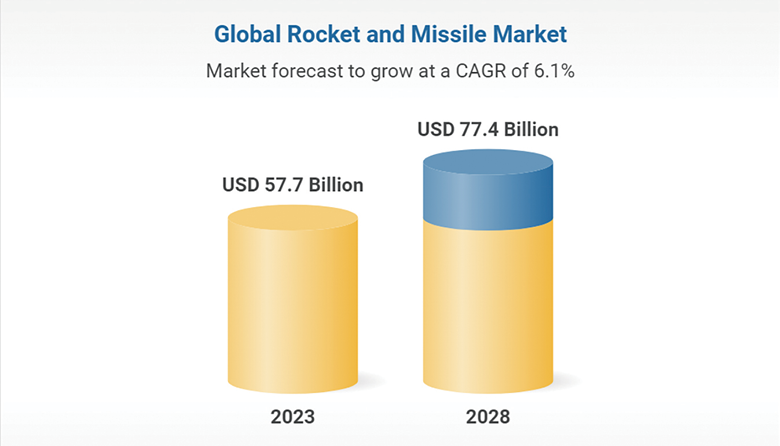

The global rocket and missile market size is projected to grow from $57.7 billion in 2023 to $77.4 billion by 2028, at 6.1% CAGR according to ResearchAndMarkets.com.

The rocket and missile market is expected to grow due to consistent increase in defense budgets across the globe and the need for advanced rockets and missiles to counter modern combat threats. Increasing conflicts and high defense spending are major factors driving the market globally.

The U.S., China, India, and Russia are spending heavily on modernizing their military resources. Many weapon manufacturers are shifting their focus toward developing precision-guided munitions.

North America is projected to be the largest regional share of the rocket and missile market during the forecast period. Major U.S. companies such as Northrop Grumman Corp., Lockheed Martin, Raytheon Technologies, and General Dynamics Corp. are investing in the R&D of new and advanced MMDS technology.

The missile segment, divided into cruise missiles and ballistic missiles, is projected to reach $60.43 billion by 2028.

The rocket market has been segmented into subsonic, supersonic, and hypersonic. Hypersonic rockets are equipped with a propulsion system to enable them to attain a speed of Mach 5 or higher, which is 5x faster than the speed of sound. Hypersonic precision-guided weapons are difficult to counter due to their high speed. Currently, these weapons are in development and expected to be operational in the near future.

Top 10 growth opportunities in defense for 2024 according to Research and Markets:

Missile defense

Counter unmanned aerial systems

Directed energy weapons

Hypersonic missiles

European defense initiatives

Military unmanned vehicles

Cloud-based test software

Open-source C2 systems

Maintenance, repair, and overhaul (MRO)

Asia-Pacific defense initiatives

Mortar systems and ammunition

For nearly a century, mortar weapon systems have remained the same, making them less appealing compared to other areas of the defense market. However, they’re gaining renewed interest due to their integration on armored and light vehicles to provide networked operations, mobility, and protection against threats found in high-intensity warfare environments.

The combined mortar systems and ammunition market is projected to grow to $25.67 billion by 2032, with a CAGR close to 3% according to Market Forecast.

Despite competition from loitering munitions, mortar systems and ammunition will continue to be an important asset in modern warfare.

The ammunition market is undergoing fundamental changes due to the amount of ammunition used in Ukraine, which highlighted the lack of preparedness of major industrial players to address the intense requirements of large-scale conventional warfare.

Countries, organizations, and the European Union are investing political and economic capital to quickly shift production and assets toward the war effort. Despite the cooperative effort in certain cases, states tend to maintain independent production lines of mortar systems and ammunition as national interest is always at the core of their economic and defense policy planning.

Armored vehicles/counter-IED vehicles

The military armored vehicles and counter-improvised explosive device (IED) vehicles market is expected to grow by $6.86 billion between 2023 and 2028, according to Technavio Research. The market will grow at 3.71% CAGR during the forecast period. The market is segmented by infantry fighting vehicle (IFV), armored personnel carrier (APC), main battle tank (MBT), self-propelled howitzer (SPH), and others; mobility type (wheeled and tracked); and geography (Asia-Pacific, North America, Middle East and Africa, Europe, and South America).

Unmanned aerial systems

The Teal Group’s 2023/2024 World Military Unmanned Aerial Systems (UAS) Market Profile & Forecast estimates UAS procurement funding will increase from a little more than $14 billion worldwide in 2024 to $23.1 billion in 2033, totaling $186.8 billion during the next 10 years. Military UAS research spending would add another $71.8 billion over the decade.

Small arms

The global market for small arms estimated at $8.7 billion in 2022 is projected to reach $10.8 billion by 2030, growing at a CAGR of 2.7% according to Research and Markets. Rifles are projected to record 2.9% CAGR and reach $5.9 billion by 2030. Growth in the pistol segment is estimated at 2.5% CAGR.

The small arms market in the U.S. was estimated at $3.8 billion in 2022. China, the world’s second largest economy, is forecast to reach a projected market size of $1.1 billion by 2030 at a CAGR of 3.6%. Among the other noteworthy geographic markets are Japan and Canada, each forecast to grow at 2% and 2.4%, respectively, from 2022 to 2030. Within Europe, Germany is forecast to grow at approximately 2.6% CAGR. Key companies in small arms market:

BAE Systems Plc

General Dynamics Corp.

BAE Systems Inc.

GC Precision Developments Pty Ltd.

Browning, Heckler & Koch GmbH

Colt’s Manufacturing Co. LLC

Glock GmbH

Herstal SA and Daniel Defense Inc.

Daniel Cleary, President, Mitsui Seiki USA

Dan Cleary, President, Mitsui Seiki USA

Manufacturing trends for 2024

In the current manufacturing landscape, the requirements for stand-alone and assisted automation are becoming increasingly evident, prompting a critical evaluation of one's position in this transformative tide. Engaging in conversations with clients and stakeholders has unveiled a consensus: the automation paradigm is here and one must decide whether to ride its wave or risk being left in the dust by competition domestically and internationally. In this discernment, without efficiencies that are next to nirvana, there exists very little middle ground; this market necessitates devising strategies to maintain cost competitiveness within an exceedingly cost-conscious market.

Automation has ascended to the zenith of priorities for many, yet the challenge lies in the intricate process of implementation. Not everyone possesses the expertise to navigate this technological shift seamlessly. Consequently, a reliance on industry partners and subject matter experts becomes imperative: individuals and entities who specialize in the nuances of automation and applications support.

Mitsui Seiki stands as a beacon among machine tool suppliers and partners, where we’ve built the foundation of our business being adept at crafting innovative solutions. Recognizing the pivotal role of automation in cost reduction, quality enhancement, and the support of heightened production demands, Mitsui Seiki comprehends the intricacies associated with human and equipment capacities. The overarching sentiment suggests automation is a collective consideration, but the daunting question prevails: where does one embark on this transformative journey?

Delving into the complexities, it becomes evident that the era of off-the-shelf commodity solutions is no longer sufficient. To be clear, automation isn't new. How and where it’s implemented has now become the key factor. A nuanced approach is requisite – a tailored solution addressing the unique challenges posed by automation. These are the conversations anticipated to burgeon, especially as industries undergo restructuring in response to cases of a new demographic of decision makers at the original equipment manufacturer (OEM) level and the more recent geopolitical shifts. The return of manufacturing operations to the U.S., particularly in the aerospace and military sectors, accentuates the need for comprehensive strategies to navigate the evolving landscape. Tier One and Tier Two suppliers should be actively sketching new business growth strategies.

As geopolitical factors compel a reevaluation of strategies, the resurgence of manufacturing in the U.S. is palpable, notably within the aerospace and military domains. Automation emerges as a linchpin for companies aiming to assert cost competitiveness in an environment acutely attuned to expenditure. The crux of successful adoption lies in forging partnerships with industry experts who comprehend the intricate interplay of automation in cost reduction, quality augmentation, and the facilitation of heightened production demands.

The market tension is palpable as Tier One suppliers and other stakeholders seize the opportunity presented by reshoring efforts. However, the stringent specifications mandated by OEMs in the aerospace and military sectors underscore the necessity of close collaboration with automation and top tier machine tool suppliers. This collaborative synergy is pivotal for the seamless integration of automation into reshoring endeavors, ensuring not only competitiveness but also resilience in the face of evolving market dynamics.

The global automatic weapons market size is projected to grow from $8.62 billion in 2023 to $13.83 billion by 2030, at a CAGR of 7% during the forecast period, according to Fortune Business Insights. MarketsAndMarkets puts the automatic rifles projection at 7.82% CAGR through 2023. Growth in the machine guns segment is expected to reach 8.7% CAGR.

The automatic weapons market in the U.S. was estimated at $2.8 billion in 2022. China, the world’s second largest economy, is forecast to reach $4.7 billion by 2030, with a CAGR of 13.1% through 2030. Japan and Canada are each forecast to grow at 3.7% and 7% respectively 2022 to 2030. Germany is forecast to grow at approximately 4.7% CAGR.

Key companies for automatic weapons:

BAE Systems

Barrett Firearms Mfg.

China North Industries Corp.

Colt’s Manufacturing Co. LLC

Denel Land Systems

FN Herstal

General Dynamics Corp.

Heckler & Koch AG

Israel Weapon Industries (IWI) Ltd.

Kalashnikov Concern

Arms manufacturers

While almost every industry has shown increases in demand or is projecting increases in the near future, the largest arms manufacturers aren’t seeing a dramatic increase in revenue.

The Stockholm International Peace Research Institute (SIPRI) reports the combined revenues of the world’s top 100 arms and ammunition manufacturing companies increased by only 3.5% in 2022 and in 2021, it was 1.9%.

The total revenue of U.S. companies fell by 7.9% to $302 billion. Lockheed Martin, the top-ranked company according to SIPRI, fell 8.9%, Raytheon fell 12%, Boeing decreased 19%, General Dynamics down 5.6%, while Northrop Grumman and BAE Systems, the 3rd and 6th ranked companies, respectively, felt no change.

SIPRI believes pandemic-related supply chain disruptions and labor shortages are still to blame for the minimal increases, but the Ukraine war and the Gaza Strip conflict should help demand surge and clear out backlogs soon.

Larry Robbins, President, Commercial Division, SMW Autoblok

Larry Robbins, President, Commercial Division, SMW Autoblok

Trends in defense & ammunition manufacturing

The ever-changing world of defense and munitions manufacturing offers specific and unique workholding challenges. Some of the most critical challenges are material diversity, precision requirements, complex geometries, and adherence to strict regulations for safety and quality control. These factors demand advanced and adaptable solutions to ensure efficient and accurate production processes.

Because of our product diversity, and complete offering, we give many options for the above requirements to be met, through flexibility and years of experience in this arena. SMW Autoblok Corp., has been providing solutions for workholding in the defense and munitions manufacturing markets since 1942.

The conflicts globally and domestically sadly show no signs of slowing down so military spending and firearms manufacturing continue to increase even if arms manufacturers aren’t currently feeling their revenues match the demand.

About the author: Jake Kauffman is managing editor for GIE Media’s Manufacturing Group of magazines. He can be reached at jkauffman@gie.net.